Chesapeake Energy (CHK) could be representing significant value at current levels, despite being up over 100% for the year. CHK has battled numerous issues in the past few years, but seems to have reinvented itself through a step change in innovative completions techniques and financial discipline. As a result, CHK could be on the verge of a real turnaround, and investors who have been loyal throughout the downturn may finally be seeing some reward.

Chesapeake SnapshotTrading at under 5x earnings (snapshot below), CHK is a steal at current share prices. When factoring in production growth of 11% quarter over quarter, CHK��s 5x multiple is more than a fair price to pay for earnings.

Source: E*TRADE

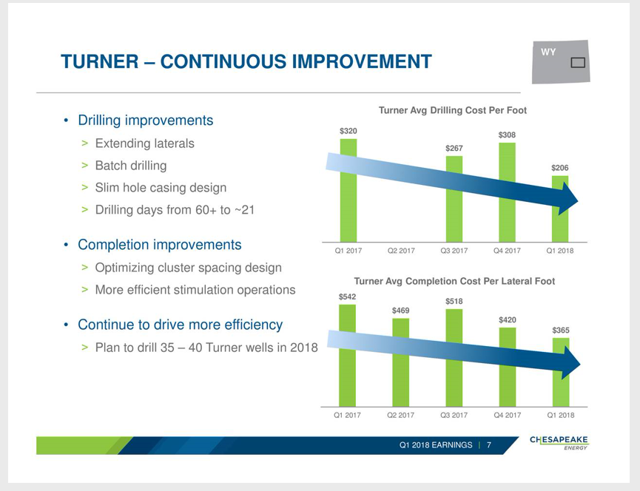

The 11% production growth has been attributed to innovations in completions techniques, such as pad drilling, longer laterals, reduced drilling times, and slim hole casing designs (reducing the hole and casing sizes for each hole interval).

Some wells, like the Sundquist 9 (below), are even averaging more than 500 barrels of oil after the first year of production. Most short cycle plays experience significant drop-offs in production after a year.

Source: Chesapeake Energy

Source: Chesapeake Energy

So, since most wells cannot produce these kinds of numbers after a year, CHK may have actually unlocked a game-changing technique for short cycle economics, and the oil and gas industry, as a whole.

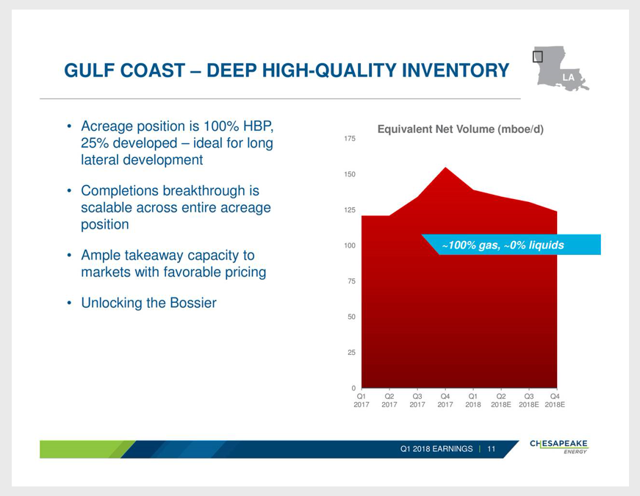

Bossier Showing Economics Similar To HaynesvilleAside from other high growth areas that CHK is benefitting from, like the Marcellus, Powder River, and Eagle Ford basins, the Bossier in Louisiana is producing excellent results.

Laterals are being started at 10,000 feet in the Bossier, and sand pumped has reached a staggering 4,000 pounds per lateral foot. Again, these techniques are learnings being applied from the Haynesville, just north of the Bossier, where a 15,000 foot lateral was recently drilled.

Source: Chesapeake Energy

Source: Chesapeake Energy

If the 15,000 foot lateral is successful in the Haynesville, those teachings can be transferred to the Bossier for eventual lateral extensions, as well (seen above).

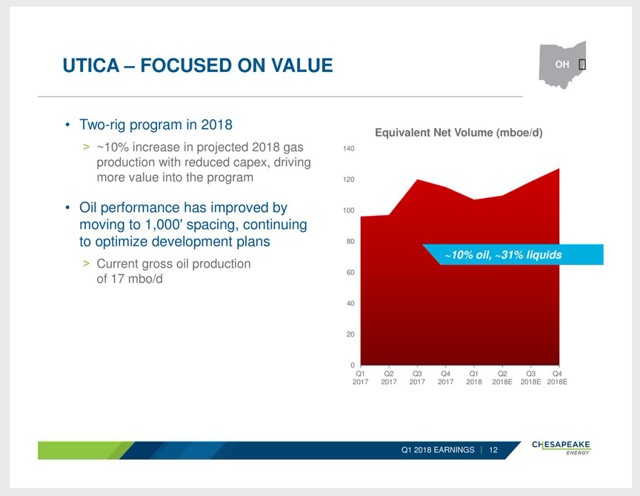

Haynesville A Working Model For UticaSimilar to the way that learnings can be applied from the Eagle Ford to the Austin Chalk by a company like EOG Resources (EOG), Chesapeake is applying learnings from the Haynesville and Eagle Ford to new completions programs in their Utica plays.

We have changed some of the landing within the Utica. We are drilling longer laterals in the Utica. We have upspaced in the Utica, because we believe that we're effectively stimulating more rock and don't need the tight spacing.

Source: Chesapeake Energy

Source: Chesapeake Energy

In fact, CHK��s outperformance in the Utica has been due to both the drilling and completion sides of the company pushing the envelope. On the drilling side, CHK focused on redesigning casing strings and lowering times to drill. On the completion side of the company, CHK experimented with pumping different fluids and using more sand, up to 33% more, in fact, which was successful in the Haynesville.

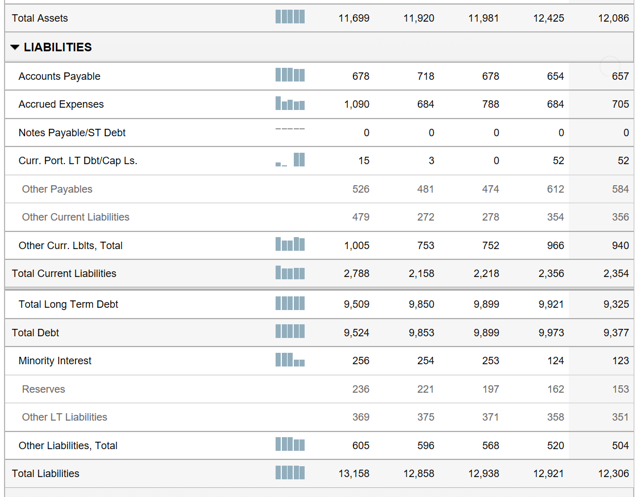

Financials Shaky But TroughingA first glance at Chesapeake��s financials are enough to make investors run for the hills. The company has more total liabilities than total assets, which is definitely a red flag. Debt levels also stand at over $9 billion, which is twice more than CHK��s market cap.

Source: E*TRADE

Source: E*TRADE

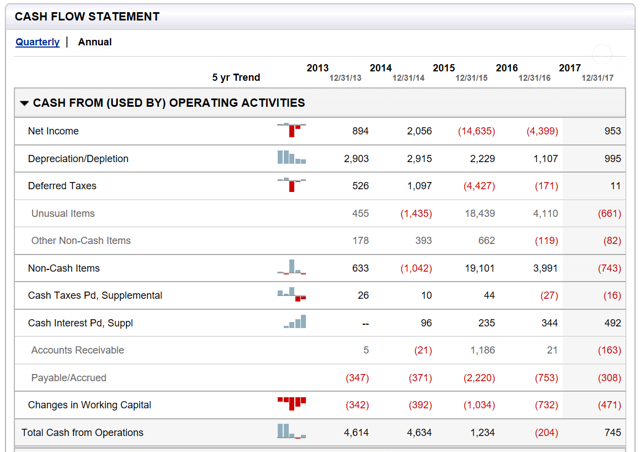

However, free cash flow did come in at $609 million, which allowed CHK to materially pay down debt by $581 million. With 100 wells expected to be popped next quarter, compared to 60 last quarter, cash flow could be almost double, which could be used to pay down additional debt.

While debt levels may be burdensome, CHK is proving they can make stellar returns with oil prices at current levels, judging by their cash flow statement below. As investors can see, income has turned positive again after the downturn experienced during 2014-2016.

Source: E*TRADE

Source: E*TRADE

Net income levels have reached pre-crash levels again, mainly because breakevens have fallen from $70 per barrel, pre-crash, to around $35 per barrel in 2018, due to the improvements in completions designs stated above. Just to get an idea of the efficiencies gained, a four-rig program in today��s operational landscape can do the same job that a ten-rig program could do in years past.

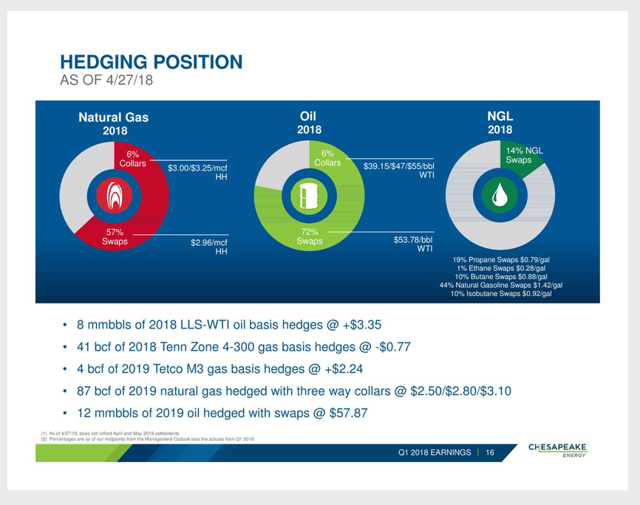

Differentials A Non-FactorLast but not least, Chesapeake is even seeing improved differentials, despite their solid growth in oil and gas volumes, which should shield the company from any future bottleneck risks. In addition, 63% of nat gas production is hedged at $2.96 per mcf, and 78% of all remaining oil volumes have been hedged at $53.78.

Source: Chesapeake Energy

Source: Chesapeake Energy

Chesapeake even took advantage of the recent spike in oil prices to hedge more than 11 million barrels of oil in 2018 at over $57 per barrel. So, while Chesapeake is not unhedged like Continental (CLR), earnings should be less volatile next year, should oil prices decide to take a dive.

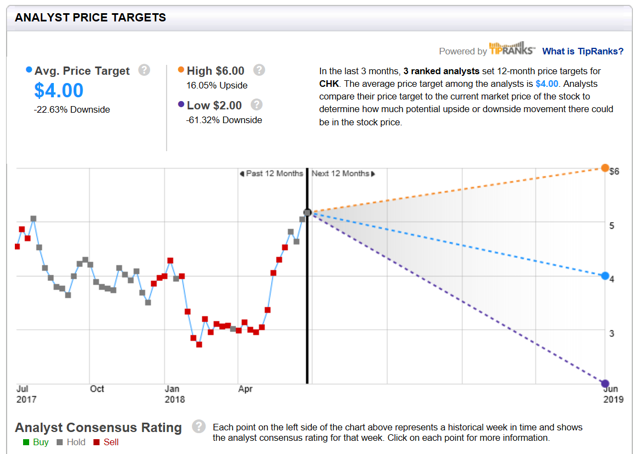

Analysts ConsensusAnalysts are not very bullish on Chesapeake, at the moment. Understandably so, debt numbers are so high that it wouldn��t take much in the way of interest rates rising or oil prices falling to derail CHK��s fragile recovery.

Source: E*TRADE

Source: E*TRADE

However, if completions results can perform consistently, and efficiencies can continue to be realized from higher production, then revenues can continue to increase at a steady enough rate to grow the company while still paying down debt.

ConclusionEven after being up over 100% for the year, Chesapeake is still trading at an attractive valuation. Due to a breakthrough in completions designs using pad drilling, more sand per lateral foot, less string casing, and longer laterals, CHK is in the midst of a turnaround and should be driving record production for the foreseeable future.

Strong hedges and improved differentials should also reduce volatility going forward for CHK, and cash flows being generated at current WTI prices should be enough for the company to retire debt in a meaningful way. As a result, investors who have stayed patient throughout the downturn could finally be rewarded for their wait.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

No comments:

Post a Comment